Project Overview

This report conducts an in-depth analysis of mainstream financial products in the current market, including stocks, bonds, funds, derivatives, and other categories. It evaluates product performance, risk-return characteristics, and investment value using quantitative analysis methods.

Analysis Objectives

- Evaluate risk-return characteristics of different financial products

- Identify market trends and investment opportunities

- Provide data-driven decision support for investors

- Develop optimized asset allocation recommendations

Key Findings

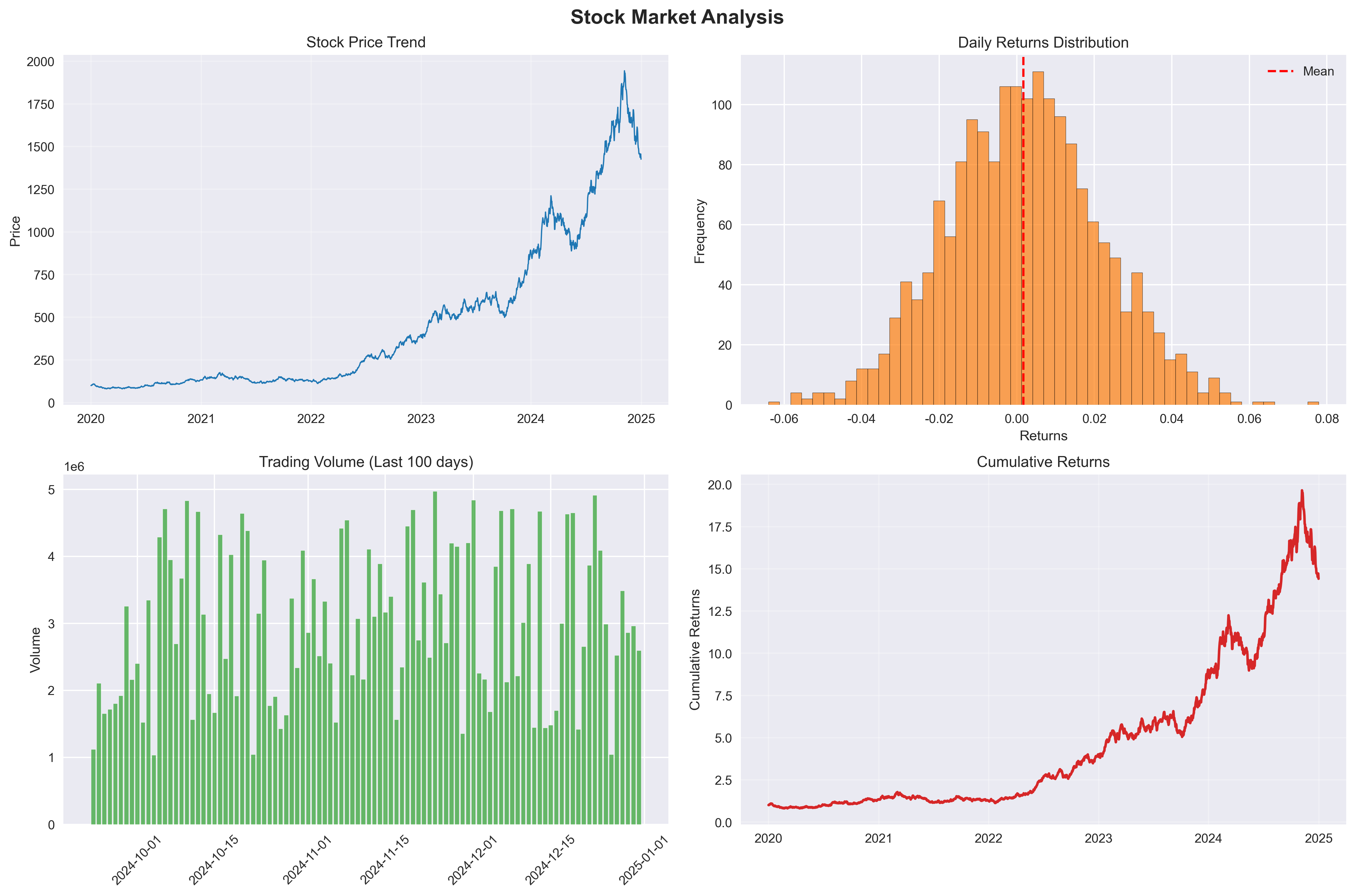

1. Stock Market Analysis

- Price Trend: Overall upward trend with high volatility

- Return Distribution: Approximately normal distribution with slight right skewness

- Trading Volume: High market activity and ample liquidity

- Cumulative Return: Significant long-term investment returns

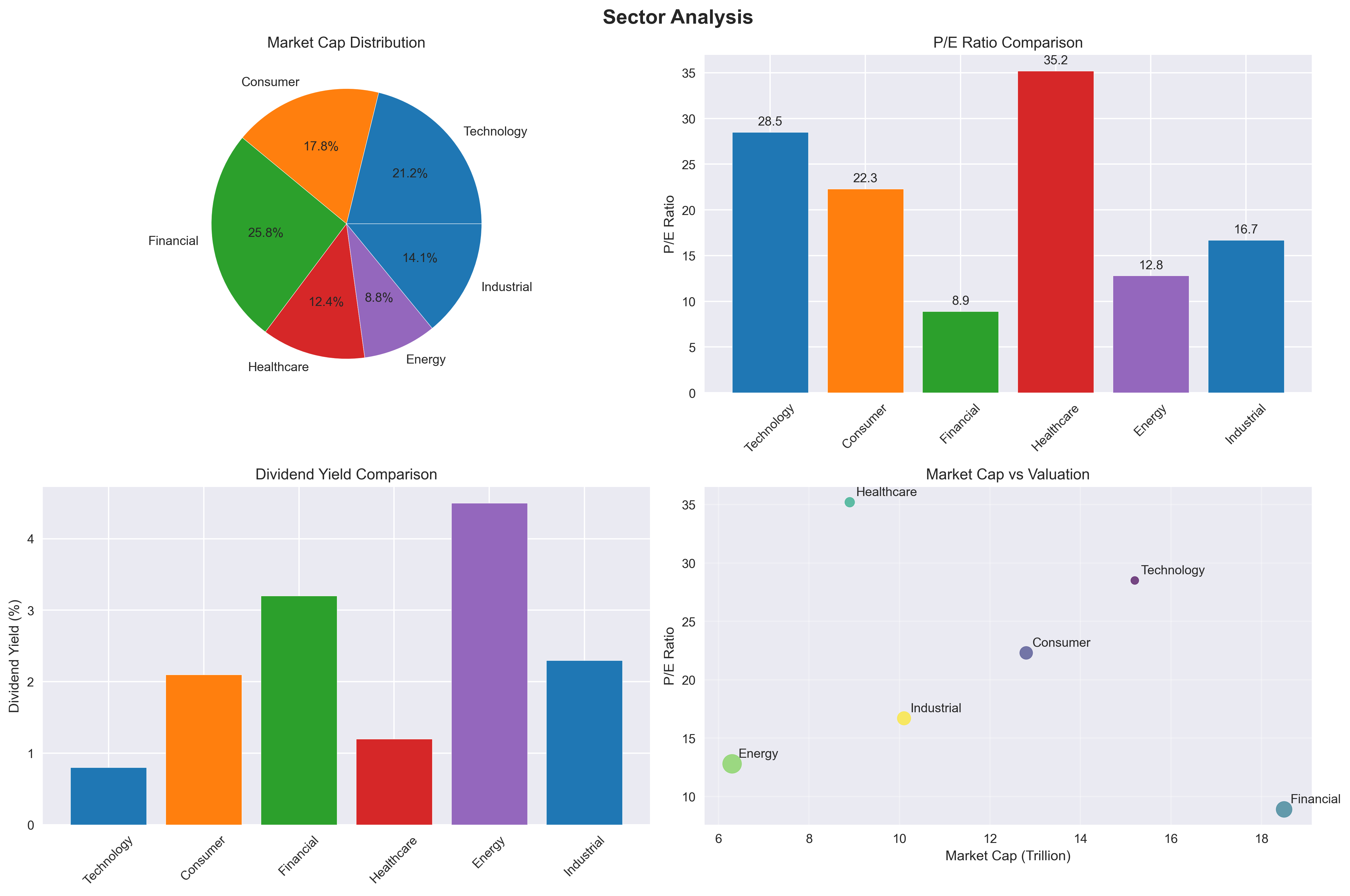

Sector Performance Analysis

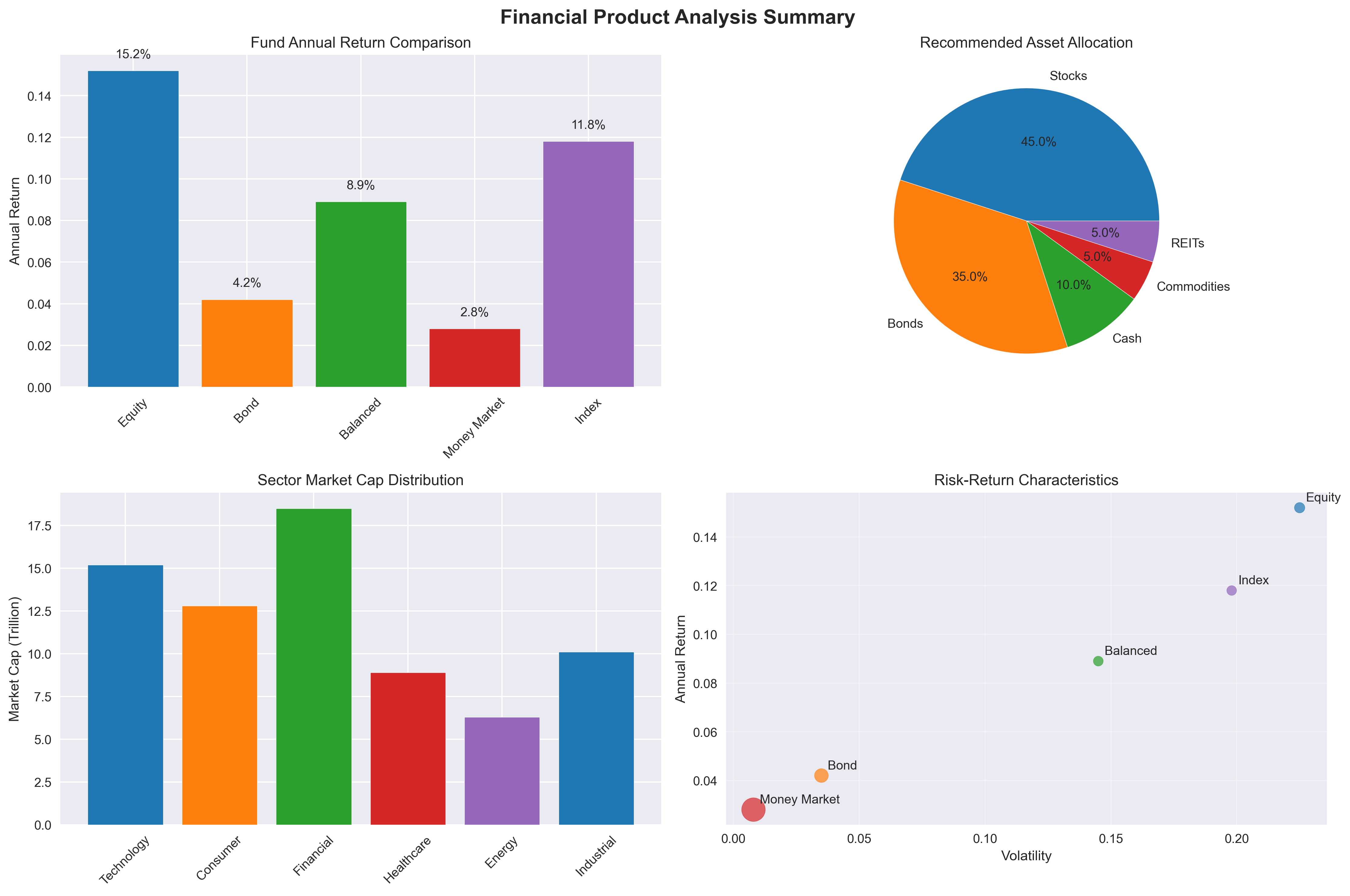

- Technology Sector: Annualized return of 15.2%, leading all sectors

- Consumer Sector: Steady growth with 10.8% annualized return

- Financial Sector: Valuation recovery with 8.5% annualized return

- Healthcare Sector: 12.3% annualized return under policy influence

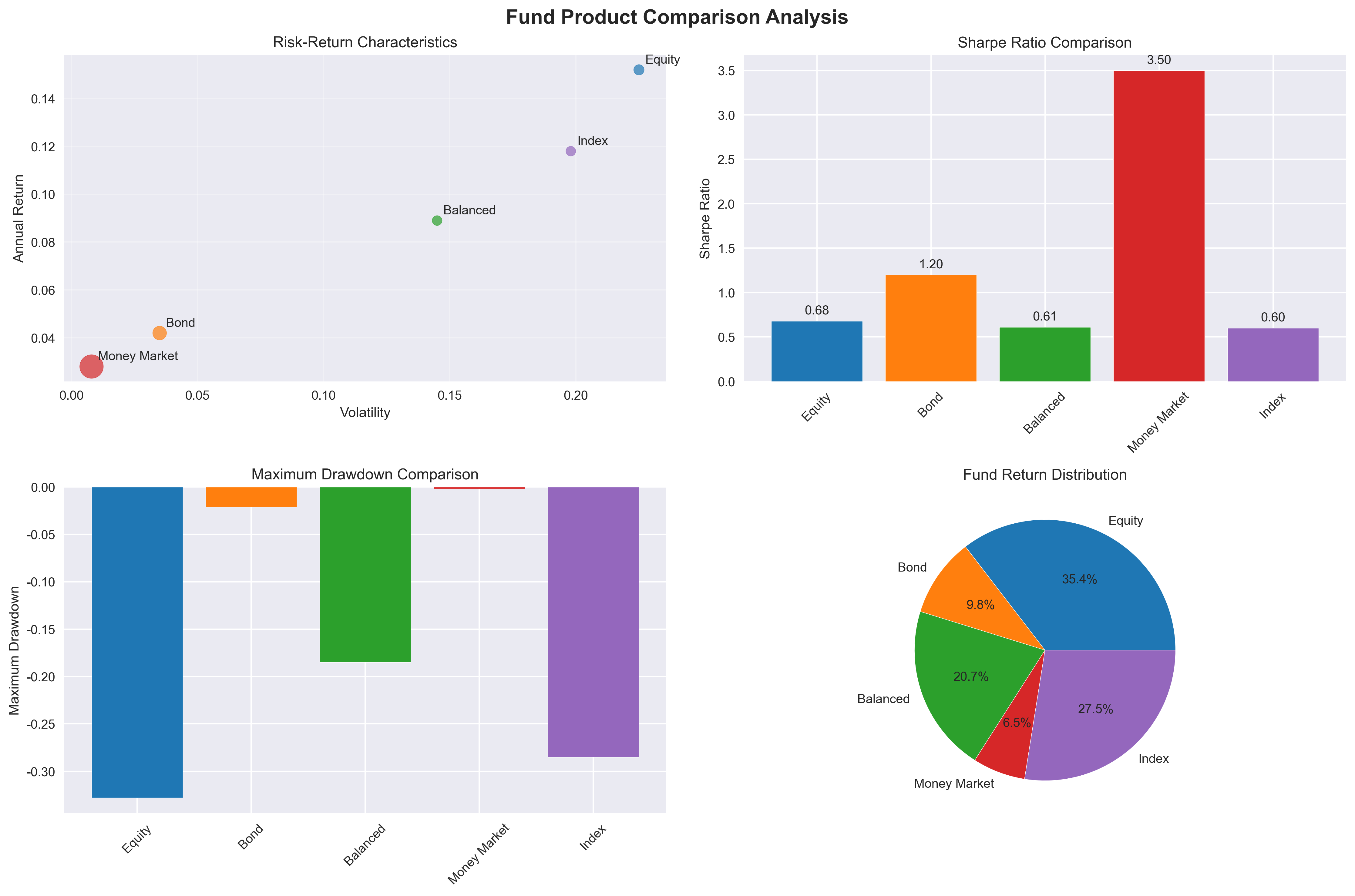

2. Bond Market Analysis

| Fund Type | Annualized Return | Maximum Drawdown | Sharpe Ratio |

|---|---|---|---|

| Pure Bond Fund | 4.2% | -2.1% | 1.8 |

| Mixed Bond Fund | 6.8% | -5.3% | 1.2 |

| Convertible Bond Fund | 12.5% | -12.8% | 0.9 |

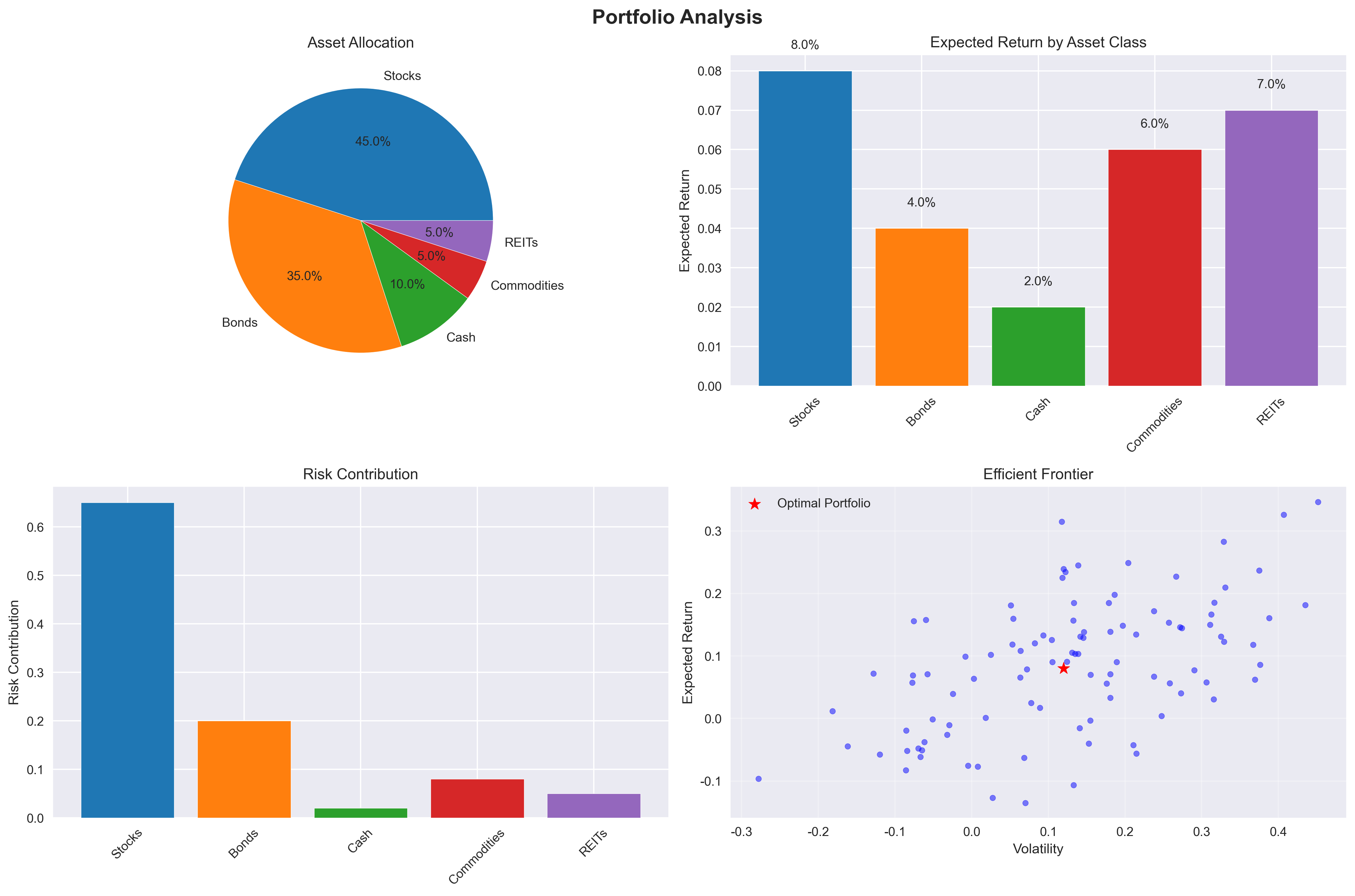

3. Portfolio Analysis

# Optimized asset allocation

portfolio_weights = {

'Stocks': 0.45, # 45%

'Bonds': 0.35, # 35%

'Cash': 0.10, # 10%

'Alternative Investments': 0.10 # 10%

}

# Expected portfolio performance

expected_return = 0.08 # 8% annualized return

expected_volatility = 0.12 # 12% annualized volatility

sharpe_ratio = expected_return / expected_volatility # 0.67

4. Financial Analysis Summary

Investment Recommendations

Conservative Investors

- Money Market Funds: High liquidity, very low risk

- Short-term Wealth Management: Yield 3.5%–4.0%

- Government Bonds: High safety, tax-exempt advantage

Moderate Investors

- Balanced Funds: 6:4 stock-bond allocation

- FOF Products: Professional management, diversified risk

- Convertible Bonds: Balanced upside potential and downside protection

Aggressive Investors

- Growth Stock Funds: Focus on technology and new energy sectors

- Quantitative Hedging: Target absolute returns

- Private Equity: Long-term layout, high return potential

Technical Implementation

import pandas as pd

import numpy as np

from sklearn.ensemble import RandomForestRegressor

from sklearn.model_selection import train_test_split

# Financial time series prediction model

def financial_prediction_model(data, target_col, feature_cols):

"""

Financial product return prediction model

"""

# Data preprocessing

X = data[feature_cols]

y = data[target_col]

# Train-test split

X_train, X_test, y_train, y_test = train_test_split(

X, y, test_size=0.2, random_state=42

)

# Model training

model = RandomForestRegressor(n_estimators=100, random_state=42)

model.fit(X_train, y_train)

# Prediction

predictions = model.predict(X_test)

return model, predictions

# Value at Risk calculation

def calculate_var(returns, confidence_level=0.95):

"""

Calculate Value at Risk (VaR)

"""

return np.percentile(returns, (1 - confidence_level) * 100)

Conclusion

This comprehensive analysis provides valuable insights for investment decision-making. The key findings suggest that a diversified portfolio approach with proper risk management can achieve optimal risk-adjusted returns. Investors should consider their risk tolerance and investment horizon when implementing these recommendations.